By Francis Hodsoll and Aaron Morrow

In a series of blogs in March and April 2017, we discussed the Composite Index (CI) and the impact that solar energy facilities (solar projects) have on the calculation of the CI. In turn, we discussed some of the possible repercussions of the CI policy concerning the awarding of solar project permits.

We continue to run across fundamental misunderstandings when it comes to the impact of solar projects on the CI calculation. To offer some clarity, we have created this Blog and Excel workbook as our version of a primer on calculating the Composite Index. Our intent is to allow anyone interested—and especially local governments—to calculate the impact a solar project will have on the Composite Index of their local district.

What is the Composite Index and how is it related to solar?

First, a quick recap. The Composite Index of Local Ability-to-Pay (CI) is a methodology that the Virginia Departments of Education and Tax use to determine the portion of the local education budget to be paid by the local government. As we highlight in our blog from March 2017, the CI measures a county’s relative wealth as compared to state averages. The metrics measured provide proxies for the county’s revenue potential from taxing this wealth —including real estate value, gross income, and retail sales. Based on these measures of relative wealth or revenue potential, the state allocates educational funds in an inverse proportion to the measured relative wealth. The CI calculates these measures of wealth on per capita and per-pupil bases. As a result, local governments with greater potential revenue pay a greater portion of their educational budget. (The CI measure metrics of potential revenue and not their actual revenues because the actual revenues are a function of both wealth and the real estate tax rate which is under the control of the county.)

In the third blog of the 2017 blog series, we discuss the impact of solar projects on the CI, which begins when the Virginia State Corporation Commission (SCC) assesses the value of solar projects and reports that value to the Department of Taxation (DOT) (and to the Commissioner of Revenue for the locality). The SCC reports both the Full Value (Fair Market Value) equal to the total project costs and the Assessed Value equal to the project cost minus any state-mandated tax exemptions. The Assessed Value represents the portion of the Full Value (Fair Market Value) that the county can legally tax.

In our previous CI blog series, we demonstrated that a solar project’s contribution to local revenues will exceed the impact on state funding caused by the solar project’s impact on the CI calculation. Therefore, counties will receive a net revenue gain from these projects.

Calculation of the Composite Index Impact

According to the Joint Legislative Audit and Review Commission of the Virginia General Assembly, the CI measures each district’s ability to pay for education, through three sources of local revenue: Local True Value (the Fair Market Value of property taxed at the real property rate less all state-mandated tax exemptions), Local Adjusted Gross Income (AGI), and Local Sales Taxable Retail Sales. To standardize these measures or benchmarks of wealth, the CI calculates a series of ratios dividing each wealth measure by both the Average Daily Student Membership (ADM) and the total local population. The CI divides each of these local ratios by the state average ratio for the same wealth measure (per ADM and per total population). The CI then calculates a weighted average of the relative ratios of wealth, using the following weights: True Value equals 50%; Adjusted Gross Income equals 40%; and Sales Taxable Retail Sales equals 10%. These calculations result in the relative revenue potential on a per ADM and per total population basis. The CI then calculates a final weighted average with a two-thirds weight applied to the ADM relative wealth measure and a one-third weight applied to the total population.

The CI multiplies this final weighted relative wealth measure by 45%. Hence, a county with a weighted average wealth ratio exactly equal to the state average will pay 45% of their local education budget. While wealthier counties pay a greater share of their educational budgets, the CI caps the maximum local contribution at 80%. A locality is therefore guaranteed to receive at least 20% of its education funding from the Commonwealth.[1]

Calculating the CI, a Step-by-Step Guide

Determining the Impact of Solar on Your District’s Composite Index

SolUnesco has developed a model that calculates the impact of a solar project on a locality’s CI calculation and the resulting impact on the state funding of the locality’s educational budget. The model generates a conservative scenario. Growth in the local wealth and state wealth would over time reduce the solar project’s impact on the CI. However, this model assumes zero growth in wealth for both the local and state over the life of the project. Many factors are held constant, such as population and total school budget, to determine the proposed impact from the solar project alone.

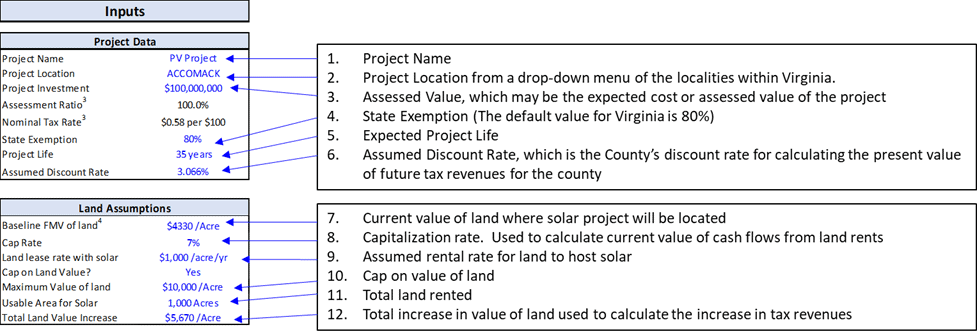

We have populated the model with the state-generated values for the following key metrics: County Taxable Real Property, Adjusted Gross Income, Taxable Retail Sales, County School Average Daily Membership (ADM), and County Population (the Static Inputs). These metrics are pulled from the Virginia Department of Education’s 2018-2020 Composite Index of Local Ability to Pay data. We have set up the model so that the user inputs 12 inputs including the projected cost of the solar project which adjusts the total value of the County Taxable Real Property. The revised taxable real property values are applied to the Virginia Department of Education’s composite index formula to compute a revised Composite Index for the county in each subsequent year.

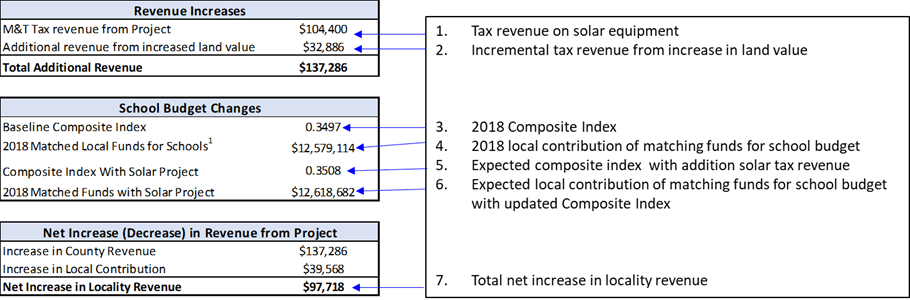

The SolUnesco model enables the user to calculate the expected impact of their project on the following tax factors: 1) the impact of increased property taxes on the local jurisdiction’s composite index; 2) the increased contribution by the local jurisdiction to the education budget; and 3) the net impact of taxes over a 25 year life of the photovoltaic system.

Running the model requires the following inputs:

Additionally the user can change assumptions for the following growth rates:

- School budgets

- County Population

- State Population

- County Enrollment

- State Enrollment

- Land Values

- Tax Revenues

- Adjusted Gross Income

Based on these inputs and the Static Inputs (described above) the The Model provides the following outputs for Year 1 and over the lifetime of the project.

Conclusion

Solar projects provide localities both quantitative and qualitative benefits such as increased county revenues, local direct and indirect investments, jobs, PR for future economic development, and decreased reliance on fossil fuels. The SolUnesco Composite Index model and this blog provide a tool for understanding the local revenue impact created by a utility-scale solar project.

Read our next blog in this series regarding increased county revenue from i) increased real property tax and ii) the rollback of the Land Use designation. The blog will explain both 1) the change to the valuation of the real property caused by these solar generation facilities; and 2) how the SolUnesco model calculates the resulting impact to the county’s Real Estate taxes.

[1] https://www.wm.edu/as/publicpolicy/documents/prs/options.pdf

[2]http://www.doe.virginia.gov/school_finance/budget/compositeindex_local_abilitypay/2018-2020/compositeindexcalc.xls

Thank you, I would like to hear more…